Government-funded buyouts after disasters are slow and inequitable – here's how that could change

- Written by A.R. Siders, Postdoctoral Fellow, Harvard University

Destructive storms like Hurricanes Florence[1] and Michael[2] prompt difficult conversations about whether to rebuild[3] or retreat[4]. Retreat is an established part of U.S. flood management: Government agencies have been paying people to move out of harm’s way[5] for several decades. But the process is flawed and needs to be improved.

Across the United States, “repetitive loss properties” that have been damaged and rebuilt multiple times using federal flood insurance payouts have cost the government, and taxpayers, more than US$12.1 billion[6]. And the challenge is growing. Rising seas due to climate change may inundate 400 to 1,100 U.S. coastal cities[7] in this century, affecting some 4 to 13 million Americans[8].

Sometimes the surest way to keep people safe is to relocate them out of the floodplain, a process called managed or strategic retreat[9]. But when I reviewed some of the largest retreat programs[10] in the United States, I found that the process is much less straightforward or fair than it should be. I also found ways to improve it.

Workers prepare a home for demolition in Spanish Grant, Texas, April 14, 2010, as part of a buyout program in the wake of Hurricane Ike.

FEMA/Patsy Lynch[11]

Workers prepare a home for demolition in Spanish Grant, Texas, April 14, 2010, as part of a buyout program in the wake of Hurricane Ike.

FEMA/Patsy Lynch[11]

Thousands of buyouts over 25 years

Since 1993, FEMA has spent just over $4 billion[12] to buy roughly 40,000 homes in 1,100 communities[13] across 44 states. The buildings are demolished and the land is required to be maintained as open space, perhaps a park or a wetland to absorb future flood waters. Other federal agencies[14] also fund buyouts.

Some whole communities have relocated. They include midwest river towns such as Pattonsburg, Missouri[15], Valmeyer, Illinois[16] and Soldiers Grove, Wisconsin[17]. According to one 2017 report, 17 U.S. communities[18] – mainly Native American – are in the process of relocating from low-lying islands and coastal areas to avoid flooding. Overall, FEMA does not have enough funding for buyouts to meet demand[19].

I recently reviewed eight of the largest U.S. buyout efforts to see how officials decided which homes to buy[20]. It was a question I’d encountered while living in New York City during and after Superstorm Sandy[21] in 2012. More than 2,500 people in New York City and state expressed interest in receiving buyouts[22], but only a few hundred received offers[23]. I wanted to know why.

New Jersey residents whose homes suffered major damage from Superstorm Sandy have diverse reactions to buyout offers in this 2014 report.Working the system

Buyouts typically are offered after disasters, when people are deciding whether to rebuild severely damaged homes and businesses or relocate away from the floodplain. Local and state governments have the authority to offer buyouts, so residents who can organize in groups and engage government agencies have the best chance of obtaining purchase offers. Officials don’t want to make offers until they’re sure a group of residents is willing to sell[24]. They want to buy up big sections of land that can be converted to parks or wetlands, rather than scattered lots that are hard to maintain.

Even when communities ask to be bought out, officials may say no based on cost[25] or potential property tax revenue losses[26]. In such cases, residents may need to organize and petition[27], as some Staten Island neighborhoods did after Sandy.

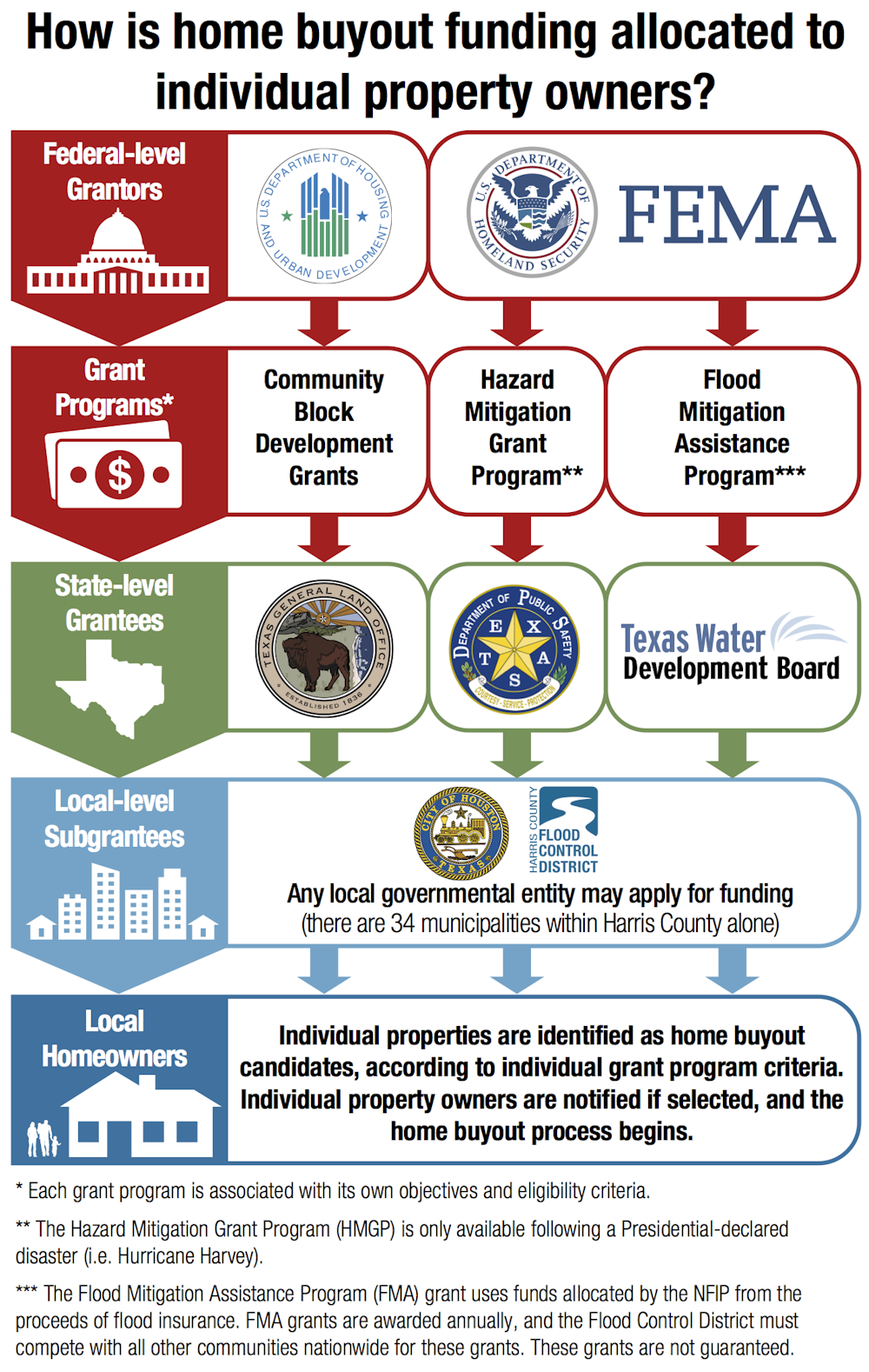

Multiple layers of government are involved in funding and awarding buyouts.

Harris County Flood Control District[28]

Multiple layers of government are involved in funding and awarding buyouts.

Harris County Flood Control District[28]

A slow and confusing process

The buyout process is not transparent. Many people struggle to figure out whether their homes are eligible, based on information from websites, press releases and public documents. Some less-than-clear criteria include: “compatibility with community and natural values[29],” and “mutual (local and state government) understanding of the benefit[30]” of the buyout.

Lack of transparency makes it hard for homeowners to make decisions[31] about whether to wait for a buyout offer, or to trust the process[32]. Even if they receive offers, it can take three to four years[33] to finalize the purchase, which is longer than many people can afford to wait after losing their homes.

Inequitable outcomes

Seemingly straightforward policies can have unintended consequences. Federal flood risk management programs are required to be “cost-effective[34]” in order to prevent overspending. However, it’s rarely cost-effective to build a $34 million floodwall[35] in front of $100,000 homes, so flood management projects like this often end up protecting wealthy areas[36]. Lower-income areas are left more exposed to damage from storms and flooding[37].

Similarly, buying out a $1 million home after a disaster makes less sense than buying 10 $100,000 homes. As a result, low-income areas are more likely to be targeted for managed retreat after disasters. These communities tend to have high numbers of minority residents, due to past discriminatory policies[38] and historic inequalities.

Helping communities that are at most risk and have the fewest resources could be a good policy, if it were done intentionally and in a way that addresses social equity. However, if these issues are not considered, flood mitigation policies can exacerbate racial and economic segregation[39] by displacing low- and middle-income residents[40] who can’t afford to spend large sums on climate-resilient homes.

Discrimination can also arise in other ways. After storms, assessors determine how much damage each house has sustained. If a house is “substantially damaged,” meaning that repairs would cost 50 percent of its assessed value, it must be relocated or elevated, which can be cost-prohibitive for owners. Low-value homes are more likely to sustain substantial damage. And owners who can’t afford to move or raise their houses may feel pressured to accept a buyout[41], although these offers are technically voluntary.

In some cases, officials have purposefully found more substantially damaged homes[42] in low-income areas. Others have chosen not to enforce substantial damage findings[43] in order to let people move back into their houses. This may seem charitable in the short term, but in the long run it leaves residents vulnerable to the next disaster.

Other researchers have found still more problems with U.S. buyouts. Purchased land is often left as derelict lots[44] because local governments lack resources to maintain it. People whose homes are purchased may relocate to other floodplains[45], or to areas that are more socially vulnerable, reducing their children’s future earning potential[46].

Worst of all, even though more than a thousand communities have participated in buyouts over 30 years, research suggests there has been little effort to learn lessons and improve these programs over time[47].

Improving the process

Managed retreat is an important tool, and will only become more so as climate change intensifies storms and flooding. But the process needs reform.

Better communication could greatly improve the buyout process. Government officials need to make decisions more transparently about where and when to retreat, and should involve communities in these decisions to improve trust in the process. Conversations about retreat should address social inequality explicitly and discuss where people might relocate. Having these discussions before disasters strike would give people time to reflect without the emotional and financial stress of post-disaster recovery. It could also speed up the buyout process.

Federal agencies should facilitate peer-to-peer learning about the innovative ways[48] some communities are using buyouts proactively to make people safer. And purchases can be structured to minimize local tax revenue losses[49].

Most importantly, Americans need to start having conversations about where federal tax dollars should be spent to protect coasts and where to retreat, before climate-driven disasters become the norm.

References

- ^ Hurricanes Florence (weather.com)

- ^ Michael (weather.com)

- ^ rebuild (thinkprogress.org)

- ^ retreat (www.vox.com)

- ^ paying people to move out of harm’s way (doi.org)

- ^ US$12.1 billion (digital.library.unt.edu)

- ^ 400 to 1,100 U.S. coastal cities (doi.org)

- ^ 4 to 13 million Americans (doi.org)

- ^ managed or strategic retreat (www.researchgate.net)

- ^ largest retreat programs (doi.org)

- ^ FEMA/Patsy Lynch (www.fema.gov)

- ^ $4 billion (www.fema.gov)

- ^ 1,100 communities (media.springernature.com)

- ^ Other federal agencies (www.hudexchange.info)

- ^ Pattonsburg, Missouri (articles.latimes.com)

- ^ Valmeyer, Illinois (www.youtube.com)

- ^ Soldiers Grove, Wisconsin (dma.wi.gov)

- ^ 17 U.S. communities (progressivereform.org)

- ^ FEMA does not have enough funding for buyouts to meet demand (www.insurancejournal.com)

- ^ which homes to buy (link.springer.com)

- ^ Superstorm Sandy (www.nhc.noaa.gov)

- ^ expressed interest in receiving buyouts (www.researchgate.net)

- ^ only a few hundred received offers (www.salon.com)

- ^ willing to sell (www.foxnews.com)

- ^ based on cost (www.myrtlebeachonline.com)

- ^ property tax revenue losses (www.redwoodtimes.com)

- ^ organize and petition (foxbeach165.com)

- ^ Harris County Flood Control District (www.hcfcd.org)

- ^ compatibility with community and natural values (www.hcfcd.org)

- ^ mutual (local and state government) understanding of the benefit (www.google.com)

- ^ make decisions (www.newsobserver.com)

- ^ trust the process (dx.doi.org)

- ^ three to four years (www.myrtlebeachonline.com)

- ^ cost-effective (www.fema.gov)

- ^ a $34 million floodwall (www.pbs.org)

- ^ protecting wealthy areas (doi.org)

- ^ more exposed to damage from storms and flooding (econpapers.repec.org)

- ^ past discriminatory policies (www.nytimes.com)

- ^ exacerbate racial and economic segregation (doi.org)

- ^ displacing low- and middle-income residents (www.insurancejournal.com)

- ^ pressured to accept a buyout (www.ijmed.org)

- ^ purposefully found more substantially damaged homes (www.ijmed.org)

- ^ chosen not to enforce substantial damage findings (www.houstonchronicle.com)

- ^ left as derelict lots (doi.org)

- ^ relocate to other floodplains (www.cakex.org)

- ^ reducing their children’s future earning potential (www.nber.org)

- ^ learn lessons and improve these programs over time (doi.org)

- ^ innovative ways (www.bloomberg.com)

- ^ minimize local tax revenue losses (riskcenter.wharton.upenn.edu)

Authors: A.R. Siders, Postdoctoral Fellow, Harvard University