Economic lookahead: As we ring in 2024, can the US economy continue to avoid a recession?

- Written by D. Brian Blank, Associate Professor of Finance, Mississippi State University

With economic forecasters rewriting their 2024 outlooks[1] following recent moves[2] from the Federal Reserve[3], The Conversation turned to two financial economists to share their thoughts on the upcoming year.

D. Brian Blank[4] and Brandy Hadley[5] are professors who study finance, firm financial decisions and the economy[6]. They explain what they’re watching in 2024.

1. At this time last year, many experts saw a downturn on the horizon. Will that long-predicted recession[7] finally come to pass in 2024?

The good news is, probably not.

The U.S. economy is not in a recession[8] and will likely continue growing[9]. Over the past year, gross domestic product has outpaced expectations[10], inflation is trending downward[11] and employment remains robust[12]. Real wages have increased[13], as has consumer spending[14]. Additionally, housing demand is strong[15] and financial markets are at all-time highs[16]. While no one should argue that there will never be another recession, 2024 seems to be an unlikely time for one[17] – unless there’s some unexpected spark like, for example[18], a new global pandemic.

To be fair, optimism leads to risk-taking, which can always contribute to the next downturn[19]. And the U.S. economy faces plenty of challenges, including already elevated debt costs[20], a possible government shutdown[21], rising consumer debt[22] and continued distress in commercial real estate[23], which could result in rolling industry downturns[24]. Other headwinds include the national debt[25], other nations’[26] weaker economies[27] and ongoing global conflict[28] and trade tensions[29].

While 2023 has seemed to many people like a “soft landing[30]” – that elusive achievement in which policymakers reduce inflation without sparking a downturn[31] – prior recessions[32] have followed periods where people thought they had been avoided[33]. That may be why bankers, finance leaders[34] and economists are still noting[35] the risks of interest rates remaining high[36].

Still, the fundamentals[37] are strong[38] and may be on the rise[39], if you believe chief financial officers[40]. Plus, despite dysfunction in Washington, recent laws and policies like the CHIPS and Science Act[41], the bipartisan infrastructure deal[42], the AI Bill of Rights[43] and the Executive Order on Safe, Secure, and Trustworthy Use of Artificial Intelligence[44] could further boost economic growth[45] by stimulating job[46] creation and enhancing competitiveness. Notably, public and private manufacturing and industrial investment are at unprecedented levels[47], and technology is quickly advancing[48], further contributing to the positive economic outlook[49], not to mention strong consumer balance sheets[50].

2. Then what about a ‘vibecession[52]’? Are we in one now, and why does it matter for 2024?

When you look at the economic pessimism revealed in polls[53] and on social media[54], a fascinating paradox emerges – despite the collective bad vibes, the majority of Americans say their personal economic situations are basically fine[55].

The writer Kyla Scanlon has called this state of affairs a “vibecession”[56]: While the economy continues to grow, the vibes are just off[57]. The fact that consumer spending continues to see sustained growth[58], despite the gloomy economic outlook[59], underscores a curious split between sentiment and economic activity.

3. What if individual income and spending keep rising? Wouldn’t that be enough to end the vibecession?

In short: Not necessarily.

While inflation has been high over the past couple of years – reaching a peak of 9.1% in June 2022 before falling to 3.1% recently[60] – most Americans have not seen their income rise as fast as inflation since 2021[61]. As a result, many are frustrated[62] that they can’t afford what they could in 2020[63]. Is reminiscing like prior generations about how Coca-Cola used to cost a nickel[64] killing the vibes? If inflation rises faster than wages in 2024, the vibes may suffer.

What’s more, other positive economic developments[65] have seemed to barely affect the vibes. Just about everyone who wants a job has one[66], which is a crucial factor in maintaining consumer confidence and spending habits.

To be sure, gas prices also play an outsized role in shaping sentiment[67], and as they unexpectedly fell in December, sentiment improved[68]. This highlights the impact of energy costs[69] on the public’s mood and suggests that fluctuations in gas prices[70] can quickly influence overall economic sentiment.

However, we suspect that consumers will keep doing what they’re doing[71] – spending money and feeling bad about the economy[72] – until some shock forces them out of it. This weird contradiction[73] between perceived gloom and personal financial well-being highlights the complex interplay of psychological factors[74] and material realities that shapes the overall economic narrative.

4. Could the vibecession become a self-fulfilling prophecy?

Consumers say they feel bad, but they’re continuing to spend more than expected[75], which has been the case[76] for more than[77] a year now[78]. These facts seem at odds with each other, and some experts worry the pessimism itself[79] could hurt the economy[80]. This is because people spend less[81] when they’re concerned about[82] the future.

However, this has been the case for months – so it’s unclear why it should change now.

While understanding[83] that consumer sentiment[84] is complex[85], we think it makes more sense to focus on what people do, not what they say. And people are behaving in a way that’s consistent with a strong economy due to rising real income[86], not to mention a robust labor market[87].

And overall, if you tell people for the better part[88] of two years[89] that a recession[90] is imminent[91], you shouldn’t be shocked that they’re gloomy[92]. If the consensus[93] is wrong[94], it should surprise no one when sentiment diverges[95] from economic data – especially with[96] politicians blaming[97] each other[98] for a weaker economy[99].

5. What else are you watching for in 2024?

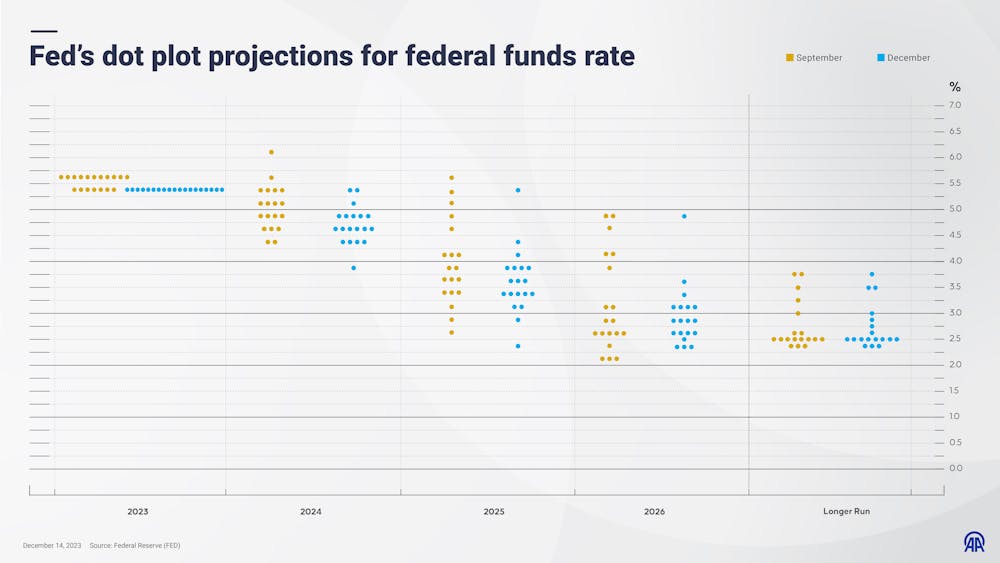

Coming off[100] the December Federal Reserve meeting[101], many forecasters[102] have rewritten[103] their 2024[104] outlooks with the[105] expectation that[106] the Fed will[107] lower rates[108] more than they anticipated before Chair Jerome Powell gave an optimistic press conference. Though many expected Powell to minimize discussions about lowering rates[109], meeting responses were strong, deeming inflation defeated and consensus expectations forecasting a benchmark federal funds rate below 4% by year end[110] to relax[111] financial conditions[112].

An infographic shows the Federal Reserve’s dot plot, which charts policymakers’ forecasts for the federal funds rate.

Omar Zaghloul/Anadolu via Getty Images[113]

An infographic shows the Federal Reserve’s dot plot, which charts policymakers’ forecasts for the federal funds rate.

Omar Zaghloul/Anadolu via Getty Images[113]

While investors appear to have overreacted[114] – again – additional slowing in inflation[115] and economic growth is likely as the economy continues to normalize post-pandemic. The most likely outcome for 2024 is that the Federal Open Market Committee lowers rates following more downward revisions to inflation data[116] beginning as early as March[117] until rates end the year just below the Fed’s 4.5% federal funds rate projection[118]. However, the Fed isn’t waiting[119] for inflation to reach its 2% target before lowering rates, which means that rapidly falling inflation could make more rate cuts possible.

Economic growth is likely to remain strong in 2024, and inflation will likely slow[120], albeit at a more muted rate. And with mortgage rates falling below 7% now[121], housing starts and mortgage originations are rising[122]. Now, housing affordability[123] may improve in the coming year[124], albeit from the worst level in decades.

While 2024 is likely[125] to involve debates in other areas[126], hopefully fewer of these[127] economic conversations will happen in 2024 than in 2023[128]. And if we are lucky, markets will rise at least as quickly[129], though we should remember that almost everyone was wrong last year – and if there’s one prediction we can make with confidence, it’s that at least some of[130] today’s forecasts[131] will look pretty silly[132] in retrospect[133].

References

- ^ economic forecasters rewriting their 2024 outlooks (www.bloomberg.com)

- ^ following recent moves (www.bloomberg.com)

- ^ from the Federal Reserve (www.schwab.com)

- ^ D. Brian Blank (scholar.google.com)

- ^ Brandy Hadley (scholar.google.com)

- ^ finance, firm financial decisions and the economy (www.sciencedirect.com)

- ^ long-predicted recession (www.forbes.com)

- ^ not in a recession (www.c-span.org)

- ^ continue growing (www.bloomberg.com)

- ^ gross domestic product has outpaced expectations (www.whitehouse.gov)

- ^ inflation is trending downward (www.usnews.com)

- ^ employment remains robust (www.cbsnews.com)

- ^ Real wages have increased (finance.yahoo.com)

- ^ consumer spending (www.bbc.com)

- ^ housing demand is strong (www.reuters.com)

- ^ all-time highs (www.washingtonpost.com)

- ^ 2024 seems to be an unlikely time for one (www.wsj.com)

- ^ spark like, for example (www.gspublishing.com)

- ^ which can always contribute to the next downturn (calvinrosser.com)

- ^ already elevated debt costs (www.businessinsider.com)

- ^ a possible government shutdown (thehill.com)

- ^ consumer debt (fredblog.stlouisfed.org)

- ^ continued distress in commercial real estate (www.nber.org)

- ^ rolling industry downturns (www.schwab.com)

- ^ the national debt (www.forbes.com)

- ^ other nations’ (twitter.com)

- ^ weaker economies (www.eastasiaforum.org)

- ^ ongoing global conflict (www.spglobal.com)

- ^ trade tensions (www.economist.com)

- ^ soft landing (twitter.com)

- ^ without sparking a downturn (www.cnn.com)

- ^ prior recessions (www.sciencedirect.com)

- ^ where people thought they had been avoided (www.nytimes.com)

- ^ finance leaders (www.bloomberg.com)

- ^ still noting (x.com)

- ^ the risks of interest rates remaining high (twitter.com)

- ^ the fundamentals (www.whitehouse.gov)

- ^ are strong (www.richmondfed.org)

- ^ may be on the rise (www.bloomberg.com)

- ^ if you believe chief financial officers (twitter.com)

- ^ CHIPS and Science Act (www.congress.gov)

- ^ bipartisan infrastructure deal (www.congress.gov)

- ^ AI Bill of Rights (www.whitehouse.gov)

- ^ Executive Order on Safe, Secure, and Trustworthy Use of Artificial Intelligence (www.whitehouse.gov)

- ^ boost economic growth (www.atlantafed.org)

- ^ stimulating job (www.mckinsey.com)

- ^ unprecedented levels (www.whitehouse.gov)

- ^ quickly advancing (www.stateof.ai)

- ^ positive economic outlook (www.marketplace.org)

- ^ strong consumer balance sheets (fred.stlouisfed.org)

- ^ Photo by Liu Jie/Xinhua via Getty Images (www.gettyimages.com)

- ^ ‘vibecession (www.nytimes.com)

- ^ revealed in polls (www.conference-board.org)

- ^ social media (www.nytimes.com)

- ^ Americans say their personal economic situations are basically fine (www.nytimes.com)

- ^ writer Kyla Scanlon has called this state of affairs a “vibecession” (www.bloomberg.com)

- ^ the vibes are just off (kyla.substack.com)

- ^ continues to see sustained growth (fred.stlouisfed.org)

- ^ gloomy economic outlook (ca.finance.yahoo.com)

- ^ inflation has been high over the past couple of years – reaching a peak of 9.1% in June 2022 before falling to 3.1% recently (www.usbank.com)

- ^ most Americans have not seen their income rise as fast as inflation since 2021 (twitter.com)

- ^ many are frustrated (www.conference-board.org)

- ^ they can’t afford what they could in 2020 (www.bloomberg.com)

- ^ about how Coca-Cola used to cost a nickel (www.wbur.org)

- ^ other positive economic developments (twitter.com)

- ^ everyone who wants a job has one (fred.stlouisfed.org)

- ^ outsized role in shaping sentiment (www.theatlantic.com)

- ^ sentiment improved (www.sca.isr.umich.edu)

- ^ energy costs (trends.google.com)

- ^ fluctuations in gas prices (www.wsj.com)

- ^ consumers will keep doing what they’re doing (kahlerfinancial.com)

- ^ and feeling bad about the economy (civiqs.com)

- ^ weird contradiction (thehustle.co)

- ^ highlights the complex interplay of psychological factors (www.theatlantic.com)

- ^ continuing to spend more than expected (fortune.com)

- ^ has been the case (www.reuters.com)

- ^ for more than (www.cnbc.com)

- ^ a year now (www.usnews.com)

- ^ worry the pessimism itself (kyla.substack.com)

- ^ hurt the economy (www.richmondfed.org)

- ^ people spend less (doi.org)

- ^ concerned about (www.nytimes.com)

- ^ While understanding (www.mercatus.org)

- ^ that consumer sentiment (www.convenience.org)

- ^ is complex (news.gallup.com)

- ^ consistent with a strong economy due to rising real income (twitter.com)

- ^ robust labor market (www.bls.gov)

- ^ tell people for the better part (www.worldbank.org)

- ^ two years (money.usnews.com)

- ^ a recession (www.bloomberg.com)

- ^ is imminent (time.com)

- ^ they’re gloomy (ca.finance.yahoo.com)

- ^ the consensus (www.wsj.com)

- ^ is wrong (www.forbes.com)

- ^ sentiment diverges (podcasts.apple.com)

- ^ from economic data – especially with (youtu.be)

- ^ politicians blaming (www.cnn.com)

- ^ each other (thefulcrum.us)

- ^ weaker economy (www.politico.com)

- ^ Coming off (www.wsj.com)

- ^ the December Federal Reserve meeting (www.bloomberg.com)

- ^ many forecasters (t.co)

- ^ have rewritten (twitter.com)

- ^ their 2024 (twitter.com)

- ^ outlooks with the (www.bloomberg.com)

- ^ expectation that (twitter.com)

- ^ the Fed will (twitter.com)

- ^ lower rates (twitter.com)

- ^ many expected Powell to minimize discussions about lowering rates (www.regions.com)

- ^ expectations forecasting a benchmark federal funds rate below 4% by year end (twitter.com)

- ^ to relax (twitter.com)

- ^ financial conditions (twitter.com)

- ^ Omar Zaghloul/Anadolu via Getty Images (www.gettyimages.com)

- ^ appear to have overreacted (twitter.com)

- ^ additional slowing in inflation (www.foxbusiness.com)

- ^ lowers rates following more downward revisions to inflation data (twitter.com)

- ^ beginning as early as March (www.cmegroup.com)

- ^ Fed’s 4.5% federal funds rate projection (twitter.com)

- ^ the Fed isn’t waiting (www.federalreserve.gov)

- ^ Economic growth is likely to remain strong in 2024, and inflation will likely slow (podcasts.apple.com)

- ^ mortgage rates falling below 7% now (www.bloomberg.com)

- ^ are rising (twitter.com)

- ^ housing affordability (www.resiclubanalytics.com)

- ^ improve in the coming year (twitter.com)

- ^ 2024 is likely (abcnews.go.com)

- ^ debates in other areas (theconversation.com)

- ^ fewer of these (www.bloomberg.com)

- ^ 2024 than in 2023 (twitter.com)

- ^ markets will rise at least as quickly (twitter.com)

- ^ at least some of (www.ft.com)

- ^ today’s forecasts (biancoresearch.com)

- ^ look pretty silly (www.cnbc.com)

- ^ in retrospect (www.calculatedriskblog.com)

Authors: D. Brian Blank, Associate Professor of Finance, Mississippi State University